The Playbook by GammaEdge #1: Why We Pin Around a Strike

Hey there trader, and welcome!

This newsletter is an extension of our Discord and is where you should expect educational content we think is relevant to your trading and investing journey.

The long-form writing here will allow us to delve deep into topics that are often too difficult to address via our other social media platforms.

While we may have specific topics we want to address, we encourage you to provide topics of interest, follow-up questions, and any other feedback as you see fit (both good and bad); we’ll be on the lookout for those at contactus@gammaedge.us.

Lastly, we appreciate your valuable time and hope we return an equal amount of value to you.

Happy Trading,

GammaEdge Team

Q: Why does the market “pin” around certain strikes? Related: why do certain gamma strikes become a “price magnet?”

A: In a word: structure.

We pin because of structure. We hover around a level because of structure.

Structure matters, so we better understand it and learn how to recognize it to leverage it in our trading and investing.

The latest JPM hedge fund roll completed on 12/30/22 had a structure that was supportive of holding the markets around the 3835 strike in the SPX.

The most common question is “how” did it pull us to this strike? Another common question is “how do we recognize this may happen in the future?”

Let’s look into the “how” and then we’ll look into things to watch for.

Large open interest (OI) exists throughout the SPX option structure. The structure has four important components that we know influence the pinning or magnet process:

The magnitude of OI at a given strike, as in the number of contracts that are open,

The magnitude of net delta at a given strike, which is influenced by a number of parameters and is multiplied by OI,

The distance between the large delta strike and spot price, which impacts delta and gamma, and

The time to expiry of the contracts at the large OI level.

OI, delta, gamma, and time to expiry underly the structure and quantify these four components. OI directly multiplies the effect of delta and gamma – as OI increases, so do net delta and gamma levels for the associated calls and puts. As spot price rolls across a large OI level, the influence on net delta and gamma can be dramatic.

This stated, we believe that net delta matters the most.

Net delta is the net exposure that the position has to the market and similarly, the exposure that the dealer has to the market at that strike. We define net delta at a strike K for a single expiry as:

Net Delta(K) = call OI(K) * call delta(K) + put OI(K) * put delta(K)

This is important: the net delta, and that sign on the net delta, is a dominant metric that drives dealer risk. If the net delta sign is negative, dealers are positive that amount of delta and will hedge their risk flat by selling; if the net delta sign is positive, then dealers are negative that delta and will hedge flat by buying. Their response to price action is heavily influenced by the net of this exposure.

Remember that gamma is the change in delta for a given change in the spot price and is most influential near spot price and short-duration options [low days-to-expiry (DTE)]. As gamma increases, the dealer’s risk exposure is also increasing in a disproportionate way, and we think this is one of the mechanisms of pinning or having a price magnet. Gamma increases as the distance between spot and price narrows or grows less, and gamma increases as DTE → 0.

Put another way, a large net delta at strike K, coupled with a short DTE, coupled with the spot price close to strike K that maximizes gamma, all make the influence of delta/OI, spot/strike, and DTE important in the context of dealer exposure and risk.

So, as we move across a large gamma strike, the multiplying effects can be tremendous if the net delta, spot/strike, and DTE stars are aligned. It is not difficult to visualize that if a dominant strike and the adjacent strikes do not have equivalent OI, then that single large OI level (and corresponding net delta and gamma) can greatly influence dealer risk and exposure.

This is exactly the situation we had with the recent JPM hedge fund that rolled on 12/30/22. Specifically, we had:

Large OI at the 3835 strike. This large open interest was structure-based: JPM sold 44,500 calls back on 9/30/22 to fund their put spread. These contracts are largely illiquid and persist and exert their influence on the overall structure.

Net-negative delta, because these calls were short from JPM’s perspective. This was coupled with the put delta at the 3835 strike and the result was to drive the net delta even more negative, much more so than surrounding strikes.

Spot price action that was “around” the 3835 level. Day over day, the influence of gamma grew as the distance between spot price and gamma narrowed, and

JPM’s expiry/roll date for the 3835 short calls was 12/30/22. As we approached this date, gamma continued to grow, so sensitivity to changes in spot prices also were larger, forcing greater dealer response.

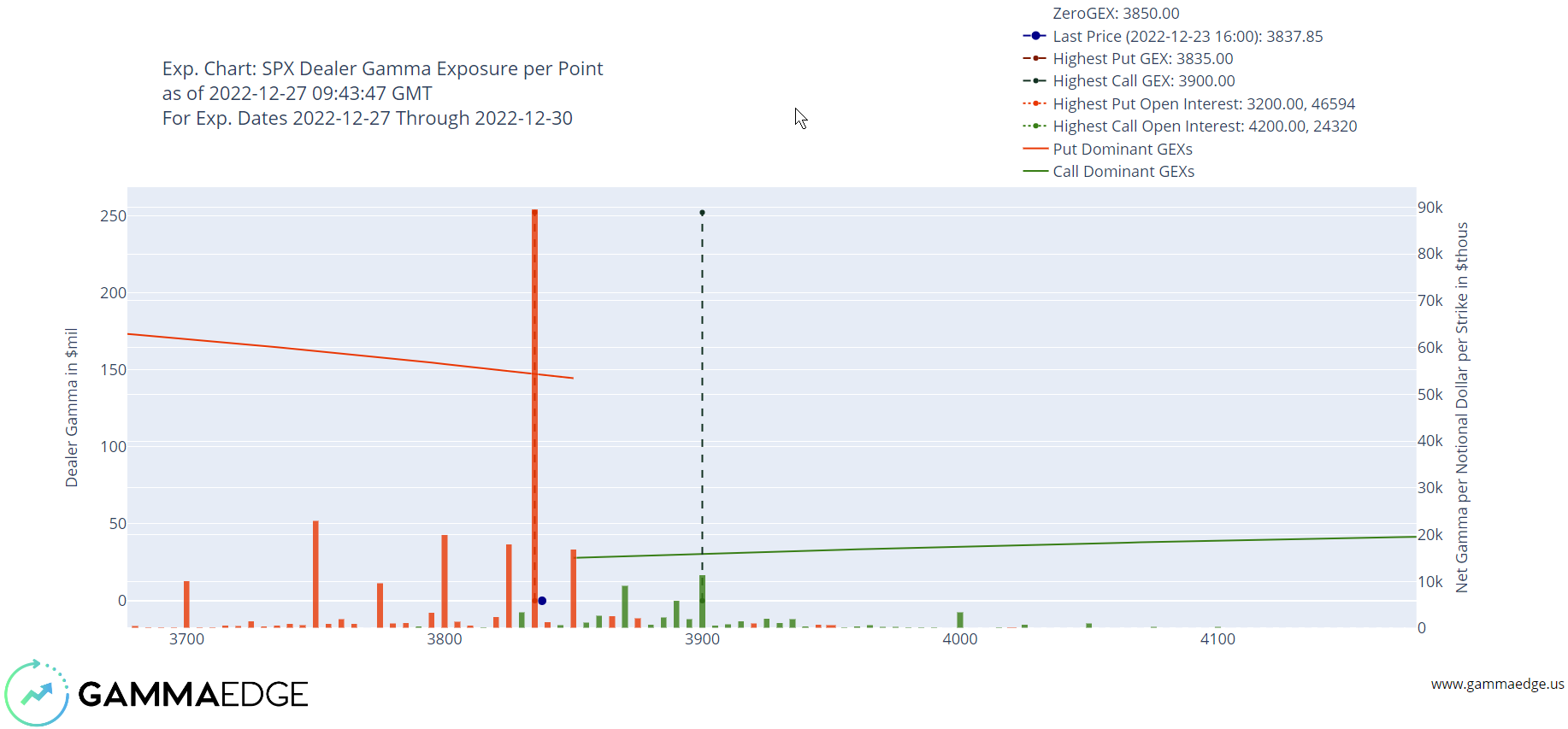

We think this latter point is important and have prepared a graphic that shows a likely cause for the pinning behavior.

The analysis is from the perspective of Tuesday, December 27th, 2022, before the market opened. We isolate the upcoming week – 12/27 through 12/30. This ability to isolate and review future outcomes is one of the core strengths of GammaEdge, and we call it our “crystal ball”.

For those already in our Discord, an equivalent Discord command, if run on the same date, would have been in the form of:

$e SPX 0 5 3675 4175

Which would have produced this chart:

Note that the graphic above shows just December 27th through the 30th. You can interact with this chart at the following link and hover over the different levels:

http://charts.gammaedge.us/SPX_0_5_zoomed_12_27_2022_04_43_12.html

The next graphic highlights the conditions that were previously described. Circle 2 shows a net-negative call OI, indicating the dominance of short calls. Between Circle 2 and Circle 3 net gamma is very negative, as is net delta notional. These conditions give rise to the setup that could lead to pinning or magnet price behavior.

Circles 4 and 5 show how prices are forced up/down to a dominant level as a function of dealer response. As prices move up (Circle 4), those short calls (net negative delta) become more ITM and drive the position toward -1 delta limit. This makes the dealer longer, pushing their deltas towards +1 limit.

All things equal, if the dealers were hedged prior to the move (a plausible assumption), they must sell to lower their delta exposure. This places downward price pressure on the structure, and we move back toward the pin level of 3835.

The opposite of this is true as prices fall (Circle 5). In this case, the short calls are now OTM, and their delta’s trend towards 0- (from the short side). Dealers correspondingly become shorter as their deltas move lower towards 0+ (from the long side). As such, the dealer response is to buy, placing upward price pressure on the markets.

A couple of key observations are also evident:

There is no other dominant gamma level around the 3835 strike for the listed expiries. This means there is no “offsetting” or “neutralizing” gamma or delta in the same time frame.

Aggregate call gamma, shown in green, is visually very small compared to the aggregate of put gamma, shown in red. This is important too: the only way to negate the influence of the 3835 strike would be to a) open a significant amount of calls at/above spot price and/or b) close a significant amount of puts at/below spot price. This did not occur as we moved through the week, but we have seen prior instances of this.

Key Takeaways:

Pay attention to JPM’s trades. The magnitude of the single-day roll at a given strike is probably material, and we should know the possible outcomes. Look for:

Large OI at a single strike, relative to surrounding strikes

Large dominance of positive or negative delta

Large influence of OI, delta, and gamma within a narrow window of expiries

Once per week, run an expiry analysis using the following commands from within the GammaEdge Discord:

$e SPX 0 7 → gives you visibility for the next 7 days

$e SPX 0 14 → gives you visibility for the next 14 days

$e SPX 8 14 → gives you visibility for the following week

We hope that you find this detail useful. Please do not hesitate to ask questions should they arise!

General Disclaimer:

You are solely responsible for your own investment/trading decisions, not GammaEdge LLC, nor any representative of GammaEdge LLC, nor any of the company’s partners.

Topics presented today, as well as in the past, are no substitute for the services of a professional investment advisor. Investment methodology and suggested approaches most likely are not appropriate for a large number of traders or investors. Discussion and presentation are made without considering your financial sophistication, financial situation, investing time horizon, or risk tolerance. You acknowledge that you are here to learn and nothing else by viewing this.

Backtesting and past performance are no guarantees of future results. Models, signals, and related analyses are for informational/educational purposes only and should not be construed as an offer to sell or soliciting an offer to buy securities. GammaEdge LLC is not registered with the U.S. Securities and Exchange Commission (neither with the securities regulatory authority or body of any state or other jurisdiction) as an investment advisor, broker-dealer, or in any other capacity does not purport to provide investment advice. Most financial instruments (stocks, bonds, funds) carry risk to the principal and are not insured by the government. Anyone viewing this session via electronic media or in person is doing so for educational purposes and does so at his or her own risk.

Data accuracy cannot be guaranteed. Opinions and analyses included herein are based on factual observations. They are believed to be reliable and produced in good faith, but no representation or warranty, expressed or implied, is made regarding their accuracy, completeness, timeliness, or correctness. Neither GammaEdge LLC, its representatives, nor its partners are liable for any errors or inaccuracies, regardless of cause, or for the lack of timeliness of, or for any delay or interruptions in, the transmission of inaccuracies to the viewers of this presentation.